End-of-Financial-Year Accounting Tips for Australian SMEs

Jun 16, 2026

Jun 16, 2026

EOFY doesn't have to be painful - here's how Australian SMEs can close the year clean, compliant, and ahead.

EOFY hits the same time every year. And yet, somehow, it still catches businesses off guard.

For a lot of business owners, EOFY means stress and an overwhelming amount of work. There are accounts to reconcile, payroll to finalise, deductions to claim, and compliance deadlines stacking up faster than they should. In 2026, the pressure is higher than usual - Payday Super launches on 1 July, STP finalisation has a firm deadline, and the ATO is matching data in real time. Getting your EOFY accounting right this year isn't just good practice. It's genuinely important.

These EOFY accounting tips won't make tax season fun. But they'll make it manageable - and they'll help you walk away paying only what you should.

Get Your Books in Order Before 30 June

Everything starts here. Your tax return, your financial statements, your deduction claims - all of it depends on your records being accurate before the year closes. This is the foundation of any solid end of financial year checklist for Australian businesses, and it begins with getting your books clean.

Reconcile Every Account

Go through every bank account, credit card, and loan account and match it against your accounting software. Check that GST coding is correct across all transactions - miscoded items create BAS discrepancies that your accountant will find months later, usually at an inconvenient time. Clear outstanding accounts payable and receivable entries, and follow up on unpaid invoices before 30 June.

Unresolved discrepancies don't disappear at EOFY. They compound. The cleaner your books are going in, the faster and cheaper your return will be on the other side.

Write Off Bad Debts Properly

If there are invoices on your books that genuinely aren't going to be paid, EOFY is the time to deal with them. The ATO allows bad debt deductions - but only if the debt is formally written off in your accounts before 30 June. That means updating your accounting software and documenting the write-off properly. A mental note doesn't count.

Do Your Stocktake and Asset Review

If your trading stock value exceeds $5,000, the ATO requires a physical stocktake at year-end. Count it, value it accurately, and record it. While you're at it, review your depreciating assets. Identify anything that might be eligible for an immediate deduction under the instant asset write-off - which we'll cover shortly.

Claim What You're Entitled To: EOFY Tax Tips That Actually Move the Needle

EOFY isn't just a compliance deadline. It's your best opportunity in the calendar year to legitimately reduce your tax bill. Here are the EOFY tax tips that make the most meaningful difference for Australian SMEs.

Instant Asset Write-Off 2026

For the 2025–26 income year, eligible businesses with an aggregated annual turnover under $10 million can immediately deduct the full cost of qualifying assets up to $20,000. Instead of depreciating the asset over several years, you claim the whole thing this financial year.

The critical detail: the asset must be installed and ready for use by 30 June 2026. Delivery alone doesn't qualify. If equipment arrives on 29 June but isn't operational until 2 July, your deduction shifts to FY27. If you're planning a purchase to capture this write-off, move now and make sure installation is completed before the month closes.

Eligible assets include tools, machinery, computers, office furniture, and other items used for genuine business purposes.

Prepay Deductible Expenses Before 30 June

The ATO's 12-month rule allows SMEs to prepay certain expenses before 30 June and claim the full deduction in the current financial year - provided the prepayment period doesn't extend beyond 30 June 2027. Insurance premiums, software subscriptions, trade memberships, and rent are all candidates.

If you're going to pay these expenses anyway, paying them before 30 June pulls the deduction forward by a full year. It's one of the simplest and most underused EOFY tax tips available to small businesses.

Get Your Super in Before the Deadline

Superannuation contributions are only deductible in the year the fund actually receives the money - not when you send the payment. If you're contributing through a clearing house, factor in processing time. The practical cutoff for most businesses is around 24 June 2026: Miss that window and your deduction moves to FY27.

If you're a business owner making personal concessional contributions, the same rule applies. Pay early, confirm receipt, and don't leave it to the last week of June.

Payroll and Compliance: What's Different in 2026

This section carries more weight this year than it has in a long time. Two significant changes are hitting Australian employers simultaneously, and both have direct EOFY implications for small business accounting in Australia.

STP Finalisation 2026: Don't Miss the 14 July Deadline

Every employer must complete their Single Touch Payroll finalisation declaration by 14 July 2026. This is your formal declaration to the ATO that wages, PAYG withholding, and reportable superannuation contributions reported through STP for the financial year are accurate and complete.

It directly affects your employees. Until you finalise STP, their income statements aren't marked as tax-ready. That means their tax returns can't be pre-filled, and they can't lodge until you act. Late STP finalisation is one of the most common sources of employee frustration during tax season - and it reflects on the business regardless of the reason for the delay.

Do it before 14 July. It takes less time than dealing with the complaints if you don't.

Payday Super 2026: Your Last Quarterly Cycle Starts Now

From 1 July 2026, quarterly superannuation ends. Under Payday Super, employers must pay super on the same day as wages, with the contribution required to clear the fund within seven business days. The ATO will monitor compliance using STP data in real time. Late contributions trigger an automatic Superannuation Guarantee Charge - there's no grace period.

This EOFY is your final quarterly super cycle. Treat it with that in mind. Reconcile your payroll records now, confirm your superannuation balances are correct, and make your last quarterly contribution early enough to clear before 30 June.

More importantly: check that your payroll system and clearing house are ready to operate on the new cadence from 1 July. Businesses that carry unresolved payroll issues past 30 June will feel the impact almost immediately. The Payday Super clock starts ticking on the first pay run of the new financial year.

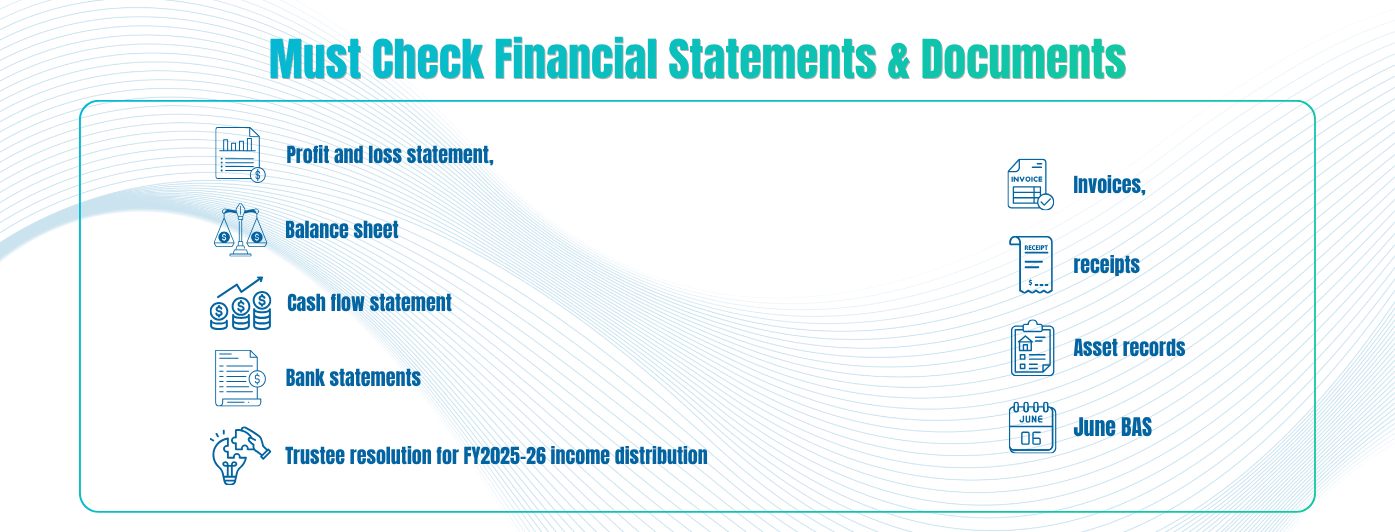

Get Your Financial Statements and Documentation Ready

Once your books are reconciled and your deductions are locked in, you need to produce and retain the right documentation. The ATO requires Australian businesses to keep financial records for a minimum of five years.

Your year-end accounting checklist for Australia should include at minimum: a profit and loss statement, balance sheet, cash flow statement, all bank statements, invoices, receipts, and asset records. If you operate a discretionary trust, the trustee resolution determining FY2025–26 income distribution must be documented by 30 June 2026. A late resolution risks the ATO taxing the entire trust income at the top marginal rate - a costly oversight for something that takes minutes to prepare.

Your June BAS is due 21 July 2026. Before lodging, reconcile your GST figures against your accounting software and confirm everything aligns with what's been reported through STP.

EOFY Is a Planning Opportunity - Use It

Most business owners treat EOFY as something to survive. The ones who get ahead of it use it as a reset.

Once your books are closed, take an hour to review FY26 properly. Did revenue hit your targets? Where did expenses run over? Are there cash flow gaps that need addressing before July? These questions are easier to answer when the numbers are fresh, and your records are clean.

More practically: assess whether your current setup can handle what FY27 demands. Payday Super changes the operational workload for any business managing payroll in-house. If your systems aren't ready, or your team is already stretched at EOFY, this is the moment to make a different decision - not in August after the first missed contribution.

Work With People Who Know EOFY Inside Out

EOFY 2026 is carrying more compliance weight than most years. STP finalisation, the final quarterly super cycle, Payday Super preparation, and the ATO's real-time data matching all land at once. The margin for error is narrower than it's been.

Hornbill helps Australian SMEs take the complexity out of EOFY - managing reconciliations, payroll finalisation, superannuation compliance, and financial reporting so you can focus on running your business rather than drowning in paperwork.